All Categories

Featured

Table of Contents

One more opportunity is if the deceased had an existing life insurance policy policy. In such instances, the marked beneficiary might receive the life insurance policy profits and use all or a portion of it to settle the mortgage, permitting them to continue to be in the home. insurance mortgagee. For people who have a reverse home mortgage, which enables people aged 55 and above to acquire a mortgage based upon their home equity, the financing rate of interest accumulates with time

During the residency in the home, no repayments are required. It is crucial for people to carefully prepare and take into consideration these elements when it involves home mortgages in Canada and their influence on the estate and successors. Looking for guidance from lawful and economic specialists can help make certain a smooth shift and correct handling of the home mortgage after the home owner's passing.

It is vital to comprehend the available choices to make sure the home loan is properly taken care of. After the fatality of a homeowner, there are a number of alternatives for home mortgage repayment that rely on numerous factors, including the regards to the mortgage, the deceased's estate preparation, and the desires of the beneficiaries. Here are some typical options:: If several beneficiaries wish to think the home mortgage, they can come to be co-borrowers and continue making the home mortgage repayments.

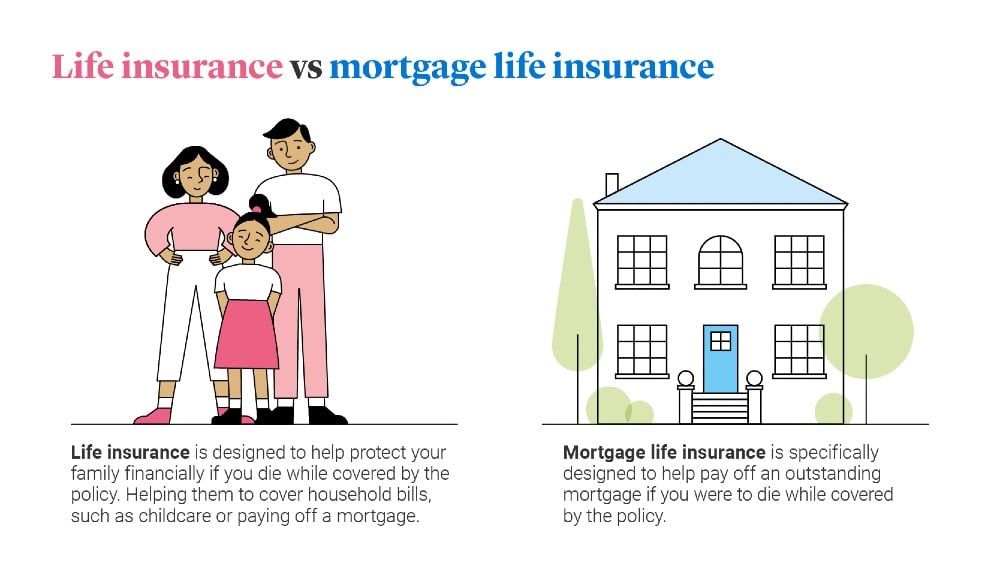

This option can provide a clean resolution to the mortgage and distribute the staying funds amongst the heirs.: If the deceased had a present life insurance plan, the marked recipient might obtain the life insurance policy earnings and utilize them to pay off the mortgage (lenders mortgage insurance definition). This can allow the recipient to remain in the home without the burden of the home mortgage

If nobody proceeds to make home mortgage repayments after the house owner's death, the home mortgage creditor can confiscate on the home. The impact of foreclosure can vary depending on the situation. If an heir is named however does not offer the residence or make the home loan settlements, the home loan servicer might start a transfer of possession, and the foreclosure can drastically damage the non-paying beneficiary's credit.In cases where a property owner dies without a will or depend on, the courts will certainly designate an executor of the estate, normally a close living family member, to disperse the properties and responsibilities.

Mortgagee Policy

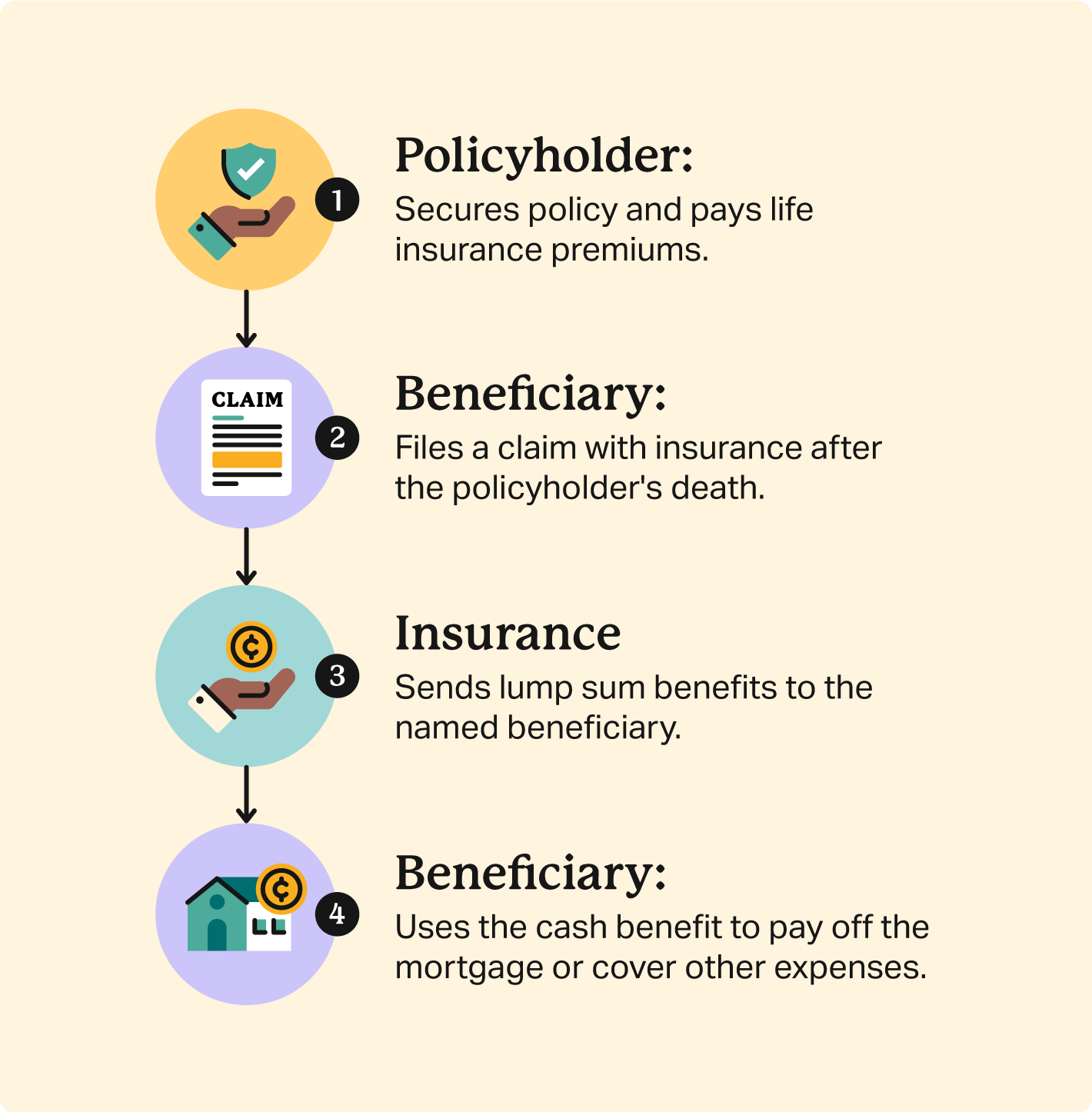

Home loan security insurance coverage (MPI) is a type of life insurance policy that is especially developed for individuals who wish to make sure their home mortgage is paid if they pass away or become impaired. Often this kind of plan is called home mortgage payment security insurance policy. The MPI process is easy. When you die, the insurance policy earnings are paid directly to your mortgage business.

When a financial institution owns the big bulk of your home, they are liable if something takes place to you and you can no more make repayments. PMI covers their risk in case of a repossession on your home (life insurance without mortgage). On the various other hand, MPI covers your danger in the occasion you can no longer make repayments on your home

The amount of MPI you need will certainly differ depending on your one-of-a-kind situation. Some elements you need to take right into account when thinking about MPI are: Your age Your wellness Your economic circumstance and sources Other types of insurance coverage that you have Some people might assume that if they currently possess $200,000 on their mortgage that they must purchase a $200,000 MPI policy.

Buy Mortgage Protection Insurance Online

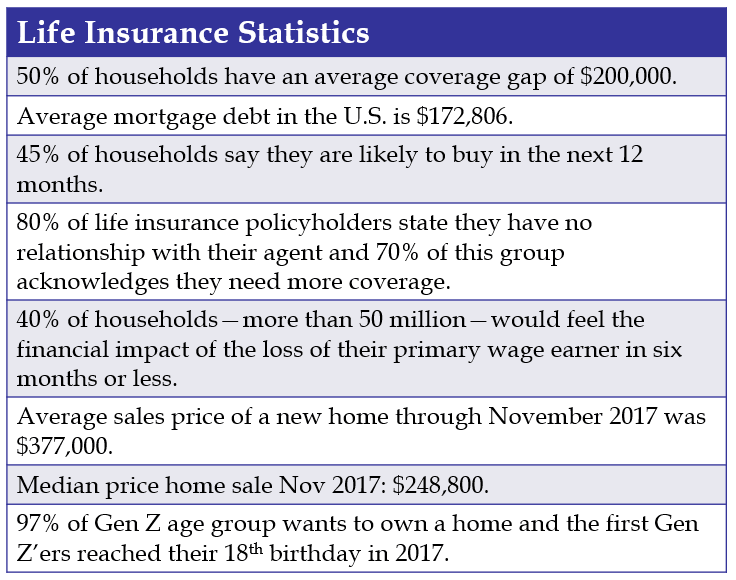

The brief answer isit depends. The concerns individuals have concerning whether or not MPI is worth it or not are the same questions they have about getting other sort of insurance policy in general. For many people, a home is our single biggest financial obligation. That suggests it's mosting likely to be the solitary biggest financial difficulty dealing with enduring relative when an income producer passes away.

The mix of anxiety, sorrow and altering family characteristics can create even the very best intentioned people to make pricey blunders. mortgage impairment definition. MPI fixes that issue. The worth of the MPI plan is straight linked to the equilibrium of your home mortgage, and insurance coverage earnings are paid directly to the bank to take treatment of the continuing to be balance

And the biggest and most difficult economic concern dealing with the surviving relative is settled instantaneously. If you have health and wellness concerns that have or will certainly produce issues for you being authorized for normal life insurance policy, such as term or whole life, MPI could be an excellent alternative for you. Normally, home loan protection insurance coverage do not need medical examinations.

Historically, the quantity of insurance policy protection on MPI plans dropped as the equilibrium on a home loan was minimized. Today, the coverage on a lot of MPI policies will certainly remain at the exact same degree you acquired. For instance, if your initial mortgage was $150,000 and you acquired $150,000 of home mortgage defense life insurance policy, your beneficiaries will certainly currently obtain $150,000 regardless of just how much you owe on your home mortgage - sell mortgage protection insurance.

If you intend to repay your home mortgage early, some insurance provider will enable you to transform your MPI plan to one more sort of life insurance policy. This is one of the inquiries you may desire to deal with up front if you are considering repaying your home early. Costs for mortgage security insurance coverage will vary based upon a variety of things.

Ppi Insurance Companies

Another element that will influence the costs amount is if you purchase an MPI plan that gives insurance coverage for both you and your spouse, supplying benefits when either among you dies or comes to be disabled. Be mindful that some companies might require your policy to be reissued if you re-finance your home, yet that's typically just the instance if you got a policy that pays out just the equilibrium left on your home loan.

What it covers is extremely narrow and clearly defined, depending on the alternatives you choose for your certain plan. If you pass away, your mortgage is paid off.

For home loan security insurance, these kinds of additional coverage are added on to policies and are understood as living benefit cyclists. They enable plan holders to tap into their home mortgage defense advantages without passing away.

For cases of, this is normally currently a totally free living benefit offered by a lot of business, but each business specifies benefit payouts differently. This covers illnesses such as cancer cells, kidney failing, cardiovascular disease, strokes, brain damage and others. globe life home mortgage group reviews. Business generally pay out in a round figure depending upon the insured's age and intensity of the disease

Sometimes, if you use 100% of the allowed funds, after that you used 100% of the plan fatality benefit value. Unlike a lot of life insurance policy plans, purchasing MPI does not call for a medical examination a lot of the time. It is offered without underwriting. This implies if you can not get term life insurance coverage due to a health problem, an assured concern home loan defense insurance policy could be your best choice.

Regardless of that you make a decision to check out a policy with, you must constantly go shopping around, because you do have choices. If you do not qualify for term life insurance coverage, after that accidental death insurance coverage may make more feeling since it's guarantee concern and means you will certainly not be subject to clinical exams or underwriting.

Mortgage Insurance In Case Of Unemployment

Make sure it covers all costs related to your home loan, consisting of interest and settlements. Ask how rapidly the plan will certainly be paid out if and when the main income earner passes away.

{kind=link}

Table of Contents

Latest Posts

Final Expense Insurance Policies

Burial Coverage

Securus Final Expense

More

Latest Posts

Final Expense Insurance Policies

Burial Coverage

Securus Final Expense